-

21Jul2020

JobKeeper Scheme Changes

Government Tightens Purse Strings with JobKeeper 2.0

JobKeeper payments will be less and harder to qualify for under the next phase of the scheme.

The current $1500 per fortnight JobKeeper payment will be reduced to between $750 and $1200 per fortnight from 28 September 2020. The lower $750 rate will apply to employees working less than 20 hours a week.

As expected, Prime Minister Scott Morrison and Federal Treasurer Josh Frydenberg announced the changes on Tuesday, 21 July 2020, which will be the first part of the phasing out of JobKeeper payments by the end of March 2021.

From 4 January 2021, the rate will again fall to $1000 per fortnight and $650 for people working less than 20 hours a week. The program will run to 28 March 2021, at a further cost of $16 billion, taking the entire JobKeeper program to $86 billion.

New Eligibility Tests

New eligibility tests beyond September 2020 are expected to result in numbers of people on JobKeeper reduced from 3.5 million to 1.4 million in the December quarter and 1 million in the March quarter.

Businesses will still be required to demonstrate the required reduction in turnover – 30 per cent for businesses with turnovers of $1 billion or less, 50 per cent for those with turnover of more than $1 billion, and 15 per cent for ACNC-registered charities.

However, the government will now require businesses to demonstrate that they have suffered an ongoing significant decline in turnover using actual GST turnover, rather than projected GST turnover.

From 28 September 2020, businesses will be required to show an actual decline in turnover for the June and September quarters to qualify for JobKeeper 2.0.

From 4 January 2021, businesses will need to reassess their turnover to demonstrate that they have met the decline in turnover test for each of the June, September and December 2020 quarters.

Treasurer Frydenberg said employers would need to demonstrate that they had met the relevant decline in turnover in both the June and September quarters to be eligible for the JobKeeeper payment in the December quarter.

“Employers will need to demonstrate that they have met the relevant decline in each of the previous three quarters ending on 31 December 2020 to remain eligible for the payment in the March quarter 2021,” Mr Frydenberg said.

While there are currently 3.5 million workers covered under JobKeeper, Treasury expects the new eligibility rules to see the figure fall to just 1.4 million workers for the December 2020 quarter, before dropping to 1 million workers in the March 2021 quarter.

-

09Jun2020

Tax Time 2020 Preparation

As tax time 2020 gets closer and closer, we wanted to help our clients prepare and ensure they are ready for the important financial period ahead. The COVID-19 pandemic has thrown a curve ball, causing this year’s tax time to be a little more complex than those in the past. However, the Affinitas Accounting team has remained on top of all things tax time 2020 related to make it easier for our clients. Are you looking to prepare for tax time 2020? Find out what steps you can take below!

Preparing for Tax Time 2020

If you’re a business owner, you know how stressful tax time can be. This tax time, there is the added stress and responsibility of the Coronavirus, which has implicated every part of every Australian’s daily life – business owner or not. In order to help our clients prepare for tax time 2020, we’ve put together a list of handy hints and helpful tips to set you on the right path. Business owners and individuals looking for help with their tax time 2020 tax returns can also get in touch with any member from our helpful team for faster assistance.

Want help preparing for tax time 2020? Get in touch!

Handy Hints for Tax Time 2020 Preparation

If you are preparing for tax time 2020, it’s best to start well before 30 June 2020. This will give you enough time to gather what you need for your tax return and prevent any nasty surprises once your tax accountant is done with your yearly results. This year, the onset of COVID-19 has made tax time considerably more stressful and given business owners and individuals alike a lot to think about and prepare for. With this in mind, we’ve put together a list of things to start thinking about and getting prepared to be on the front-foot for tax time 2020.

Covid-19 Claims

- If you have worked from home due to Covid-19, the government has announced that it will let taxpayers claim 80c per hour to cover costs of home office expenses, based on documented records of the hours you worked from home. However, if you do not think that this will adequately compensate for what it has actually cost you to work from home, you can choose to assess via a one-month diary establishing your percentage of expenses – mobile phone, home computers, printers, internet and any other costs related to working from home.

Individuals

- Account for all your sources of income during the year, particularly if your have had several jobs or received Centrelink benefits for part of the year.

- Make sure you have receipts for all your work related deductions. Some expenses like union fees can be taken straight from your annual PAYG summary, but most require their own receipt.

- If you have made tax deductible donations during the year, you will need receipts for these.

- If you use your car for work make sure you have a calculation of how many km you have travelled. If you require a log book, make sure that it is up to date.

- Any other work related travel expenses will require diarised notes of where and when you travelled, the purpose of the travel and receipts for fares, accommodation and any other expenses.

- Did you purchase any uniform or protective clothing for work purposes?

- Did you undertake any study that was directly related to your work activities?

- If you studied or worked from home, how many hours per week?

- If you were required to use your personal internet or mobile phone, have you made an effort to establish the percentage usage for work?

- You will need details of any earnings from bank interest, share dividends and managed funds.

- If you sold any investments you will need both purchase and sales details if there is a capital gains calculation to be completed.

- Have you checked your insurances to see if they include tax deductible income protection premiums?

Small Business Owners

- Many of the hints for individuals are transferrable to small business owners.

- Have you reviewed your debtors to see if there are any bad debts to be written off?

- Do you have any obsolete stock or equipment that can be written off prior to 30 June?

- Are all your staff obligations for PAYG Tax and Superannuation up to date?

- Have you disposed of any capital equipment or bought any new equipment?

- Is any of the new equipment worth less than $150,000 and available for immediate write-off?

- Have you sat down and completed a tax planning exercise to in the past quarter?

Investment Property Owners

- Ask for an annual statement of income and expenses from your rental property manager

- Account for all the expenses paid directly by you in relation to the property – usually rates, water, body corp, insurance and some repairs.

- Have you checked whether you have a current depreciation schedule for the property.

Virtual Visits for Tax Time 2020

Covid-19 is about to change the way many people deal with their annual tax returns. Online tax preparation is nothing new, but tax season 2020 is going to put more emphasis on professional accountants to offer flexible and virtual alternatives to face-to-face appointments.

Many taxpayers traditionally visit their accountant for an annual chat, and we look forward to this face-to-face connection at our Aspley office. But this year, visiting your tax accountants office is a risk that should be avoided by all tax professionals and their clients. Covid-19 may be contained – but it has not been cured, nor has a vaccine been developed. We don’t want to put our clients or our team at risk, if that risk can be easily avoided.

The Affinitas Accounting team will be engaging with clients via email, phone, Zoom or any other form of communication that does not involve face-to-face interaction. Affinitas Accounting has already spent many years in the online world and have prepared thousands of returns via post and/or email. This will make the transition easy for those new to such a system.

Via the tax agents portal, we already have access to much of our clients’ current and historical tax information. We have learnt how to use technology to its best advantage – including sharing our screens with clients to better explain various issues. And we are working on introducing paperless processes to allow clients to check and sign their returns – then ultimately receive their notices of assessment. Even if you have multiple years’ worth of tax returns to lodge, or a business or investment property tax return, these can be done via a virtual initial appointment and online process.

We believe many people are going to discover just how easy and convenient it is to virtually visit their accountants in 2020 – and will probably make it an annual event.

Need Help for Tax Time 2020?

The Affinitas Accounting team is dedicated to helping you manage the upcoming tax season and make the process as smooth and simple as possible. To this end, we are extending our operating hours during tax time, from July to October, to help clients or schedule virtual appointments. If you need to speak to one of our friendly tax agents, get in touch!

-

28May2020

Understanding the ATO Instant Asset Write-Off

The ATO’s instant asset write-off is another form of financial relief the ATO and the Federal Government has included and expanded on in the COVID-19 relief schemes. First developed in 2015 as a way of enabling small businesses to claim the depreciation amount of a work-related purchase like a car or a computer in one hit, rather than gradually over a number of years. Recently, the ATO expanded on the criteria needed for this asset write-off. If you are a business owner or sole trader interested in the instant asset write-off, read on to find out how the scheme works.

What is the ATO Instant Asset Write-Off?

The instant asset write-off scheme was initially introduced in 2015 and was largely aimed at helping small businesses claim the depreciation amount of company assets immediately, rather than over many years. The onset of the COVID-19 pandemic has seen the government and the ATO introduce a number of financial relief schemes aimed at helping businesses survive this troubling time, and recently, they adjusted the criteria for the instant asset write-off scheme to include larger businesses.

As part of the ATO and the government’s economic stimulus measures, the asset limit for the instant asset write-off scheme has increased from $30,000 to $150,000. The pool of eligible businesses has also been amended from those with an aggregated turnover of less than $50 million, to an aggregated turnover of less than $500 million. These significant changes will see the instant asset write-off scheme benefit many more businesses than before.

This means that a greater number of businesses can purchase a piece of equipment or a company vehicle and receive an immediate deduction of up to $150,000. However, the relief scheme is not without strict regulations that must be adhered to if businesses are to utilise this financial relief benefit to its maximum, and there is some confusion in particular around how the scheme works for company-owned and bought vehicles.

What is the ATO Instant Asset Write-Off Limit on Cars?

While the instant asset write-off limit has increased from $30,000 to $150,000, a ‘car cost limit’ has been implemented for businesses wanting to purchase a vehicle at this time. This will define the amount you can actually claim on a newly purchased vehicle.

Specifically, cars that are “designed to carry a load less than one tonne and fewer than nine passengers,” have a total claim limit of $57,581 and anything beyond that point “cannot be claimed under any other depreciation rules,” the ATO explains.

However, the full purchase price of a vehicle which can carry more than one tonne/more than nine passengers can be claimed back.

Cars that cost $150,000 or more, as well as farm trucks and tractors, are ineligible for the instant asset write-off scheme.

Does the Car Threshold Include LCT, On-Road Costs, Insurance and Registration?

All costs but insurance and registration are included in the car threshold amount – this includes stamp duty, any accessories, luxury car tax, on-road costs and delivery.

Insurance and registration are recurring business costs, which are immediately deductible under the general deduction provision and thus not included in the cost of the car.

Are Lease and Financed Cars Eligible?

A hire purchase lease will be eligible for the instant asset write-off scheme, but operating and finance leases will not qualify.

Criteria for the ATO Instant Asset Write-Off: Cars

- Must be a business asset. Any old asset will not comply. Whether it’s a new or second hand asset, to get the 100% deduction the asset must be 100% employed in your business. Assets that are part business and part private will require a log book to establish a business use percentage.

- Car limits may still apply. A passenger vehicle designed to carry a load of less than 1 tonne and fewer than 9 passengers is limited to a maximum write-off of $57,581 – even if it 100% used in business. Vehicles that are greater than one tonne or carry 9 passengers or more may be eligible for a higher write-off amount.

- You must own and be using the asset by 30 June. The asset must be owned by the business and be in use (or able to be used) by the business by 30 June to claim the write-off.

- Employees are not eligible for the instant asset write-off scheme, but they may be able to claim back some of their own car usage.

Many car dealerships are calling for the extension of the scheme to allow more businesses to take advantage of it.

Choose Affinitas Accounting

The ATO’s instant asset write-off can provide a major financial aid to many businesses. If you think you are eligible and want to apply, please feel free to contact one of our friendly business accountants for swift, prompt assistance.

-

28May2020

JobKeeper Explained: What is it and Who is Eligible?

JobKeeper was introduced in April 2020 and is an effort being made by the Federal Government to support eligible businesses effected by COVID-19 to cover the costs of their employee’s wages, on condition that the business has experienced a loss of a predetermined portion of their turnover. Around $130 billion will be paid to hundreds of thousands of Australian businesses to subsidize employee wages. If you are a business owner who wants to explore JobKeeper and want to know if you can apply, read on to find out how it works and who is eligible.

What is JobKeeper?

The Coronavirus Economic Response Package (Payments and Benefits) Act 2020 came into effect on 9 April 2020 (though the payment scheme was officially backdated to 30 March 2020), which allowed for the implementation of the Federal Government’s $130 billion JobKeeper relief scheme. It forms part of the Government’s $320 billion total economic stimulus and support package for businesses and employees affected by the Coronavirus (COVID–19) crisis. The scheme was aimed at keeping Australians employed even in the event of their employer temporarily closing down due to trading limitations caused by the outbreak.

Businesses who were impacted by COVID-19 and who suffered a loss in turnover of at least 30% can apply for the JobKeeper fund which will give them access to a wage subsidy for their employees. Eligible employers will be able to continue to pay their employees on a fortnightly basis: $1500 per employee from March 30 2020, for a maximum period of 6 months.

For those in non-essential industries, such as accommodation, retail and hospitality, this subsidy payment equates a complete wage replacement – something those working in the hardest-hit industries would need.

The JobKeeper payment scheme will end on 27 September 2020, encompassing 13 fortnights of employee wage payments.

Who is Eligible for JobKeeper?

In an effort to provide support and financial assistance to businesses and employees who need it, the Government has set out a defined list of criteria that businesses need to meet in order to apply for the JobKeeper payment scheme. The eligibility criteria are:

- Businesses that have experienced a loss in turnover of at least 30%, in a month-long period compared to last year

- Businesses that have experienced a loss in turnover of at least 50% if they usually bring in more than $1 billion annually, in a month-long period compared to last year

- Charities that have lost at least 15% of their turnover in the same period

- Applicants who have casual workers must have employed the casual worker for at least a year

- Sole traders

- Temporary work visa holders may not apply unless they are New Zealanders on the special 444 subclass visas

Sole traders and some other entities (such as partnerships, trusts or companies) may be entitled to the JobKeeper Payment scheme under the business participation entitlement. A limit applies of one $1,500 JobKeeper payment per fortnight for one eligible business participant. Sole traders, one partner in a partnership, one beneficiary of a trust, and one director or shareholder of a company may be regarded as an eligible business participant.

How do the JobKeeper Payments Work?

Eligible employers and companies will be able to claim the subsidy amount of $1500 per eligible employee on a fortnightly basis. However, the Australian Tax Office (ATO), who has partnered with the Government during this crisis, will pay employers in arrears, within 14 days of month end. The employer will continue to receive the subsidy payments for eligible employees while they are eligible for the payments. While the program is expected to run for 6 months, payments will stop if the employee is no longer employed by the business.

Monthly employer payroll reporting is required to trigger the payment by the ATO using Single Touch Payroll (STP).

JobKeeper Obligations and Risks

While the JobKeeper payment scheme is aimed at helping businesses and their employees, the system is not without risks that business owners should be aware of.

If an incorrect claim is made, or if the ATO in the future decides that you were ineligible to receive the JobKeeper payment, the ATO will require you to repay any JobKeeper payments that you have received, plus penalties and interest.

The key risks and responsibilities you, as the employer, must be aware of include:- The employer certifies the facts provided to the ATO and the JobKeeper claim made

- The employer receives significant JobKeeper payments over a 6 month period. For example, an employer with 5 employees would receive $97,500, and an employer with 10 employees would receive $195 000

- If the employer makes a mistake and is found to be ineligible by the ATO (for example, its turnover was not down by 30%), then they may have to repay all amounts received back to the ATO This is not recoverable from employees (unless they confirmed they were eligible but were not)

- An employee ceases to be eligible if they cease employment during the life of this JobKeeper scheme

- The ATO requires you to keep all records in relation to your JobKeeper claim for a 5 year period.

How to Apply for JobKeeper

The ATO has specific actions that must take place within tight time frames for an employer to receive the JobKeeper payment. If you want to apply for JobKeeper for your business, please contact us or read the below:

1. Employer Eligibility Assessment

- Review ATO requirements for the business

- Review ATO requirements for employees

- Review ATO requirements for Business Participation Entitlement – Sole Trader, Partnership, Company or Trust

- Document the fall in turnover % in case of future ATO audit

2. Identify Eligible Employees

- Prepare list of eligible employees

- Prepare JobKeeper employee nomination notice for all eligible employees and ensure

all notices are signed

3. Make Correct Wage Payments to Eligible Employees

- Ensure your payroll software is correctly set up to record JobKeeper “top up” payments

- Pay the minimum $1500 before tax to each eligible employee each fortnight (starting with the fortnight 30 March to 12 April) to be able to claim the JobKeeper payment for that fortnight

- Continue to pay the minimum $1500 to employees in every subsequent fortnight until 27 September 2020

4. Enrolment for JobKeeper

- Enrol for JobKeeper using ATO online services from 20 April 2020

- Provide employer bank account details for receipt of JobKeeper payment

- Confirm if applicant is entitled to a “Business Participation Payment”

- Specify the number of employees who will be eligible for one period and the number eligible for two periods

- Get confirmation that all employees the employer plans to nominate are eligible and the employer has notified them and has their agreement

5. Apply for JobKeeper Payments

- Apply to claim the JobKeeper payment using ATO online services between 4 May 2020 and 31 May 2020

- Ensure all eligible employees have been paid $1500 per fortnight

- Identify the eligible employees from a Single Touch Payroll prefill or by manually entering into ATO online services

- Update your accounting system Chart of Accounts to ensure JobKeeper payments are coded correctly

6. Monthly JobKeeper Declaration Report

- Using ATO online services, report to the ATO using their Monthly JobKeeper

- Declaration Report on the following:

- Reconfirm that your reported eligible employees have not changed

- Input current GST Turnover for the reporting month

- Input projected GST Turnover for the following month

- Notify if any eligible employees have changed or left your employment

Partner with Us

We want to do our part during the pandemic and, as such, are providing support and assistance to businesses who want to apply for the JobKeeper payment scheme. Please be sure to contact us if you or your business require assistance with your application.

-

22Apr2020

The Value of JobKeeper to Your Business

If you are eligible to receive the JobKeeper payment for all your eligible employees for the entire 6 month period, we have estimated that you would receive the total JobKeeper payment amount below:

This equates to $ 19,500 per employee or eligible business participant for over 6 months.

This is a great help to business cashflows during these difficult times, but as with anything involving regulation and the ATO, there is a risk…

OBLIGATIONS AND RISKS TO YOUR BUSINESS

If an incorrect claim is made or if the ATO in the future decides that you were ineligible to receive the JobKeeper payment, the ATO will require you to repay them any JobKeeper payments that you have received plus penalties and interest.

The key risks to you as the employer include:

- The employer certifies the facts provided to the ATO and the JobKeeper claim made.

- The employer receives significant JobKeeper payments for over 6 months. For example, an employer with 5 employees would receive $97,500, and an employer with 10 employees would receive $195 000.

- If the employer makes a mistake and is found to be ineligible by the ATO (for example, its turnover is not down by 30%), then they may have to repay all amounts received back to the ATO. This is not recoverable from employees (unless they confirmed they were eligible but were not)

- An employee ceases to be eligible if they cease employment during the life of this JobKeeper scheme.

Also, the ATO requires you to keep all records concerning your JobKeeper claim for 5 years.

TIMELINE OF ACTIONS YOU NEED TO TAKE

The ATO has specific actions that must take place within tight timeframes for an employer to receive the JobKeeper payment.

Employer Eligibility Assessment – NOW

- Review ATO requirements for the business

- Review ATO requirements for employees

- Review ATO requirements for Business Participation Entitlement – Sole Trader, Partnership, Company or Trust

- Document the fall in turnover % in case of future ATO audit

Identify Eligible Employees – NOW

- Prepare a list of eligible employees

- Prepare JobKeeper employee nomination notice for all eligible employees and ensure all notices are signed

Make Correct Wage Payments to Eligible Employees – NOW

- Ensure your payroll software is correctly set up to record JobKeeper “top-up” payments

- Pay the minimum $1,500 before tax to each eligible employee each fortnight (starting with the fortnight 30 March to 12 April) to be able to claim the JobKeeper payment for that fortnight

- Continue to pay the minimum $1,500 to employees in every subsequent fortnight until 27 September 2020

Enrolment for JobKeeper – FROM 20 APRIL 2020 TO BE DONE BY 30 APRIL

Enrol for JobKeeper using ATO online services from 20 April 202

- Provide employer bank account details for receipt of JobKeeper payment

- Confirm if the applicant is entitled to a “Business Participation Payment

- Specify the number of employees who will be eligible for one period and the number eligible for two periods

- Get a confirmation that all employees the employer plans to nominate are eligible and the employer has notified them and has their agreement

Apply for JobKeeper Payments – FROM 4 MAY 2020

- Apply to claim the JobKeeper payment using ATO online services between 4 May 2020 and 31 May 2020

- Ensure all eligible employees have been paid $1,500 per fortnight

- Identify the eligible employees from an STP prefill or by manually entering into ATO online services

- Update your accounting system Chart of Accounts to ensure JobKeeper payments are coded correctly

Monthly JobKeeper Declaration Report – DUE BY 7TH OF EACH MONTH

Using ATO online services, report to the ATO using their Monthly JobKeeper Declaration Report on the following:

- Reconfirm that your reported eligible employees have not changed

- Input current GST Turnover for the reporting month

- Input projected GST Turnover for the following month

- Notify if any eligible employees have changed or left your employment

- Getting this correct and done on a timely basis is essential. We can offer assistance for each of the steps above, including the monthly reporting.

Please reach out to our team for more information on (07) 3510 1500 or get in touch with us here.

What can business owners do to prepare for JobKeeper

-

25Mar2020

The Second Govt Stimulus Package: What Business Owners Need To Know

Yesterday, the Australian Federal Government delivered a substantially increased package available for individuals and small businesses. You can read the official government release here.

For those of you that prepare your own BAS, I’d recommend that you consult with us before lodging the March 2020 BAS, so we can ensure your small business avails itself of all assistance measures on offer.

Affinitas Accounting is a member of professional associations, thought leadership groups and specialist private forums. Across all of these, there have been numerous discussions as to the interpretation of how these measures will be applied. The consensus, with which we agree, is to wait until later this week to read the legislation, before advising any on any specific strategies.

While we know that not all our clients are business owners themselves, we all have friends or families within our communities who are. Please feel free to share this information with anyone you feel may benefit from it, so we can ensure we are providing support to as many people who need it as possible.

Please do feel free to reach out with any questions that you may have, and we will release an updated newsletter and video as soon as we have more information to share.

Thank you for your patience during this turbulent and anxious time for your small business.

In Summary

Business

- Tax-free payments up to $100,000 for small business and not-for-profit employers. An increase in the previously announced initial tax-free payments for employers to a maximum of $50,000. In addition to this, the second round of payments will be made up to a maximum of $50,000, accessible from July 2020.

- Solvency safety net – temporary 6-month increase to the threshold at which creditors can issue a statutory demand on a company from $2,000 to $20,000, and an increase in the time companies have to respond from 21 days to 6 months. Directors also are provided with temporary relief from personal liability for trading while insolvent for 6 months.

- Access to working capital – Introduction of a Coronavirus SME guarantee scheme protecting financial institutions by guaranteeing 50% of new loans to SMEs.

- Sole traders and self-employed eligible for Jobseeker payment – the eligibility criteria to access income support relaxed for the self-employed and sole traders.

- Temporary relief from some Corporations Act requirements

Tax-free payments up to $100,000 for employers

From: 28 April 2020

Eligibility: Small and medium business entity employers and not-for-profit entities, with an aggregated annual turnover under $50 million.

The Government has increased the previously announced measures to provide cash flow support to the business.

Now, eligible businesses with a turnover of less than $50 million will initially be able to access tax-free cash flow support, with the minimum amount being increased to $10,000 and the maximum amount increased to $50,000 (previously $2,000 to $25,000). However, additional support will be provided in the July – October 2020 period so that eligible entities will receive total minimum support of $20,000 and up to $100,000.

For a business to qualify for this support it must have been established before 12 March 2020. The rules are more flexible for charities because the Government recognises that new charities might be established in response to the pandemic.

The cash flow support measures will be provided in the form of a credit in the activity statement system.

The support will be provided in two phases:

- The first phase ensures that eligible employers receive a credit equal to 100% of the PAYG amounts withheld from salary and wages paid to employees during the relevant period, up to the maximum amount of $50,000.

- The second phase ensures that eligible employers receive another series of credits, equal to the credits that were received under the first phase. For example, if a business received $40,000 of credits in the first phase it will receive a further $40,000 of credits in the second phase. These additional credits will be spread over two or four activity statement periods, depending on whether the employer lodges on a quarterly or monthly basis.

If a business pays salary and wages to employees but is not required to withhold any tax then a minimum payment of $10,000 will be made in the first phase and a further payment of $10,000 will be made in the second phase.

The credits are automatically calculated by the ATO and employers will need to lodge an activity statement to trigger the entitlement. If the credit puts the business in a refund position the excess amount will be refunded by the ATO within 14 days.

Businesses that lodge activity statements every quarter will be eligible to receive credits in the first phase for the quarters ending March 2020 and June 2020. Credits in the second phase will be available for the quarters ending June 2020 and September 2020. The minimum $10,000 payment will be applied to the first lodgement.

A business that lodges every month will be eligible for the credits in the first phase for the March 2020, April 2020, May 2020 and June 2020 lodgements. Credits in the second phase will be available for the June 2020, July 2020, August 2020 and September lodgements. The minimum $10,000 payment will be applied to the first lodgement.

Eligibility for the measure will be based on prior year turnover. We will have to wait for the legislation for the finer details. Not-for-profit employers, including charities, with an aggregated turnover under $50 million will also be able to access the cash flow support.

Solvency safety net

A safety net has been put in place to protect businesses in temporary financial distress as a result of the pandemic by lessening the threat of actions that could unnecessarily push them into insolvency and force the winding up of the business.

These include:

- A temporary 6 month increase to the threshold at which creditors can issue a statutory demand on a company from $2,000 to $20,000.

- The time a company has to respond to statutory demands will increase from 21 days to 6 months.

- For 6 months, directors will be provided with temporary relief from personal liability for trading while insolvent.

- See also bankruptcy safety net below

It will be more important than ever for a business to stay on top of their debtors. Debts incurred will still be payable by the business. Only those debts incurred in the ordinary course of the business will be subject to the safety net measures.

Access to working capital for SMEs – supporting lenders

The Government has announced a Coronavirus SME guarantee scheme that will guarantee 50% of new loans to SMEs up to $20 billion. These loans are new short-term unsecured loans to SMEs.

SMEs with a turnover of up to $50 million will be eligible to receive these loans.

The Government will provide eligible lenders with a guarantee for loans with the following terms:

- The maximum total size of loans of $250,000 per borrower.

- The loans will be up to three years, with an initial six month repayment holiday.

- The loans will be in the form of unsecured finance, meaning that borrowers will not have to provide an asset as security for the loan.

Loans will be subject to lenders’ credit assessment processes with the expectation that lenders will look through the cycle to sensibly take into account the uncertainty of the current economic conditions.

This latest measure builds on the previous initiatives to ensure the small business can access capital, including:

- An exemption to the responsible lending obligations to enable financial institutions to provide new credit, credit limit increases, and credit variations and restructures,

- $15bn to the Australian Office of Financial Management to invest in wholesale funding markets used by small banks and non-banks to enable these lenders to support SMEs, and

- Australian Banking Association members will defer loan repayments for 6 months for small businesses (affected small businesses will need to apply for relief).

Sole traders and self-employed eligible for Jobseeker payment

The eligibility criteria to access income support payments will be relaxed to enable the self-employed and sole traders whose income has been reduced, to access support.

Temporary relief from Corporations Act requirements

The Treasurer has been given a temporary instrument-making power to amend the Corporations Act to provide relief or modifications to specific compliance obligations.

ASIC has announced measures for those companies with a 31 December financial year that need to hold their AGMs by 31 May 2020, providing a two month no action period and enabling hybrid virtual AGMs.

Bankruptcy safety net

A temporary 6-month increase to the threshold for the minimum amount of debt required for a creditor to initiate bankruptcy proceedings against a debtor will increase from $5,000 to $20,000. Also, the time a debtor has to respond to a bankruptcy notice will be temporarily increased from 21 days to six months.

Where someone declares their intention to enter voluntary bankruptcy, the period of protection from unsecured creditors will be extended from 21 days to 6 months.

More information:

-

24Mar2020

The Second $66.1 bn Stimulus Package: What Individuals and Families Need To Know

The Australian Federal Government delivered a substantially increased package available for individuals and small businesses yesterday to ease the economic downturn from the Coronavirus pandemic.

Affinitas Accounting is a member of professional associations, thought leadership groups and specialist private forums.

There have been numerous discussions across all of these as to the interpretation of how these measures will be applied. The consensus, with which we agree, is to read the legislation, before advising any on any specific strategies.

Please do feel free to reach out with any questions that you may have, and we will release updates as soon as we have more information to share.

In Summary

Individuals

- Early release of superannuation – individuals in financial distress may be able to access up to $10,000 of their superannuation in 2019-20, and a further $10,000 in 2020-21. The withdrawals will be tax-free and will not affect Centrelink or Veterans’ Affairs payments.

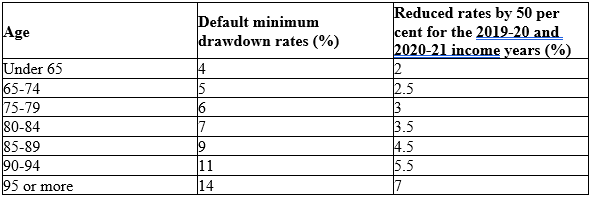

- Temporary reduction in minimum superannuation drawdown rates – superannuation minimum drawdown requirements for account-based pensions and similar products reduced by 50% in 2019-20 and 2020-21.

- Deeming rates reduced – from 1 May, superannuation deeming rates reduced further to a lower rate of 0.25% and upper rate of 2.25%.

Supplements increased, access extended and eased – for 6 months from 27 April 2020:

- A temporary coronavirus supplement of $550 will be paid to existing income support recipients (people will receive their normal payment plus $550 each fortnight for 6 months).

- A second one-off stimulus payment of $750 will be paid automatically from 13 June 2020 to certain income support recipients (in addition to the payment made from 31 March 2020).

- Eligibility for access to income support eased to include sole traders and the self-employed, and to those caring for someone infected or in isolation.

- Waiting periods and assets tests temporarily waived.

Bankruptcy safety net – temporary 6-month increase to the threshold for the minimum amount of debt required for a creditor to initiate bankruptcy proceedings against a debtor from $5,000 to $20,000.

The Government has flagged that additional stimulus packages will be required.

Sole traders and self-employed eligible for Jobseeker payment

The eligibility criteria to access income support payments will be relaxed to enable the self-employed and sole traders whose income has been reduced, to access support.

Individuals

Early release of superannuation

From mid-April, individuals in financial distress may be able to access up to $10,000 of their superannuation in 2019-20 and a further $10,000 in 2020-21. The withdrawals will be tax-free and will not affect Centrelink or Veterans’ Affairs payments.

To be eligible to access your superannuation you need to meet one or more of the following requirements:- you are unemployed; or

- you are eligible to receive a job seeker payment, youth allowance for jobseekers, parenting payment (which includes the single and partnered payments), special benefit or farm household allowance; or

- on or after 1 January 2020

- you were made redundant; or

- your working hours were reduced by 20% or more; or

- if you are a sole trader — your business was suspended or there was a reduction in your turnover of 20% or more.

For those eligible to access their superannuation, you can apply directly to the ATO through themyGov website from mid-April.

Temporary reduction in minimum superannuation drawdown rates

Superannuation minimum drawdown requirements for account-based pensions and similar products will be reduced by 50% in 2019-20 and 2020-21.

The upper and lower social security deeming rates will be reduced further. As of 1 May 2020, the upper deeming rate will be 2.25% and the lower deeming rate of 0.25%.

Time-limited fortnightly $550 ‘coronavirus supplement’

For the next 6 months, the Government is introducing a new Coronavirus supplement to be paid at a rate of $550 per fortnight. This supplement will be paid to both existing and new recipients in the eligible payment categories.

The payment will be made to those receiving:- Jobseeker payment (and those transitioning to the jobseeker payment)

- Youth allowance jobseeker

- Parenting payment

- Farm household allowance

- Special benefits recipients

Also, eligibility to income support payments will be expanded to:

- Permanent employees who are stood down or lose their job

- Casual workers

- Sole traders

- The self-employed

- Contract workers who meet the income test

The Government notes that these criteria could include those required to care for someone affected by the Coronavirus. Asset testing has also been reduced and will be waived for 6 months. Income testing will still apply.

The payment is not available if you have access to any employer entitlements such as annual or sick leave or income protection insurance.Second $750 payment to households

The Government is now providing two separate $750 payments to social security, veteran and other income support recipients and eligible concession card holders residing in Australia (see the full list here). The payment will be exempt from taxation and will not count as income for Social Security, Farm Household Allowance and Veteran payments.

Payment 1 from 31 March 2020 (previously announced on 12 March): Available to people who are eligible payment recipients and concession cardholders at any time between 12 March 2020 to 13 April 2020;

Payment 2 from 13 July 2020: Available to people who are eligible payment recipients and concession card holders on 10 July 2020.

The payments will be made automatically to those that meet the criteria.

Bankruptcy safety net

A temporary 6-month increase to the threshold for the minimum amount of debt required for a creditor to initiate bankruptcy proceedings against a debtor will increase from $5,000 to $20,000. Also, the time a debtor has to respond to a bankruptcy notice will be temporarily increased from 21 days to six months.

Where someone declares their intention to enter voluntary bankruptcy, the period of protection from unsecured creditors will be extended from 21 days to 6 months.More information: